Top 5 Reasons People Choose Equity Release [2025 Study]

Author: Gerard Boon

Managing Director at Boon Brokers

Equity Release has had mixed press over the years, but for many over 55s it provides the freedom to do things in later life that they wouldn’t otherwise be able to.

But what are homeowners planning on spending that money on? How does it vary by region or gender? And what are the main reasons those who still feel nervous about Equity Release wouldn’t consider it?

It’s no secret that Equity Release has had its fair share of negative coverage over the years. And rightly so when the products were newly launched and unregulated in the 1990s, and people were advised to take out products which were not suitable for their needs.

However, that’s a long way away from where Equity Release is now. In the last 15 years the products and the regulations surrounding lenders have tightened dramatically.

Equity Release products can help homeowners release some of the money held in their property.

Given house prices have risen by a staggering 1145 per cent since 1980, many people have a significant proportion of their wealth tied up in their home.

Although for many people there is a comfort in having something to pass on to their loved ones, for others it can seem crazy to put off doing things they want or need to do in life, because they don’t have the equivalent cash sat in a bank account.

Equity Release allows a homeowner aged over 55 to borrow between 30 and 58 per cent of the value of their home whilst allowing them to continue living in it. They can either take out a Lifetime Mortgage or a Home Reversion product and the money can be taken as a lump sum or a draw down.

Homeowners opting for a lump sum take on average a pot of £81,700 and those opting for draw down typically release around £104,500. In 2020 £3.89bn was released to homeowners in the UK from their homes via Equity Release.

We wanted to understand what the driving forces are for homeowners who might consider Equity Release. Do they need the money for general living expenses, or would they want to do something exciting with the cash?

We ran a survey with almost 1,000 homeowners aged over 55 to ask them just that.

The top 5 reasons people would use Equity Release

- To fund day-to-day retirement costs

- To help my children financially

- To travel

- To pay for home or garden improvements

- To pay off debt

It seems covering day-to-day living costs is the most common reason or helping children or family members with their finances.

Taking the money to fund travelling and holidays came next on the list and ranked as a higher priority for those aged 55 to 64 rather than those over 65.

Home and garden improvements was something many homeowners felt they would want to do with the money, which could potentially add value to the home if it needed updating. Others might need to make adjustments to their property for health reasons.

Consolidating other debts was also a reason given by some homeowners, perhaps wanting to clear off any high interest rates or wanting to cut down on monthly repayments.

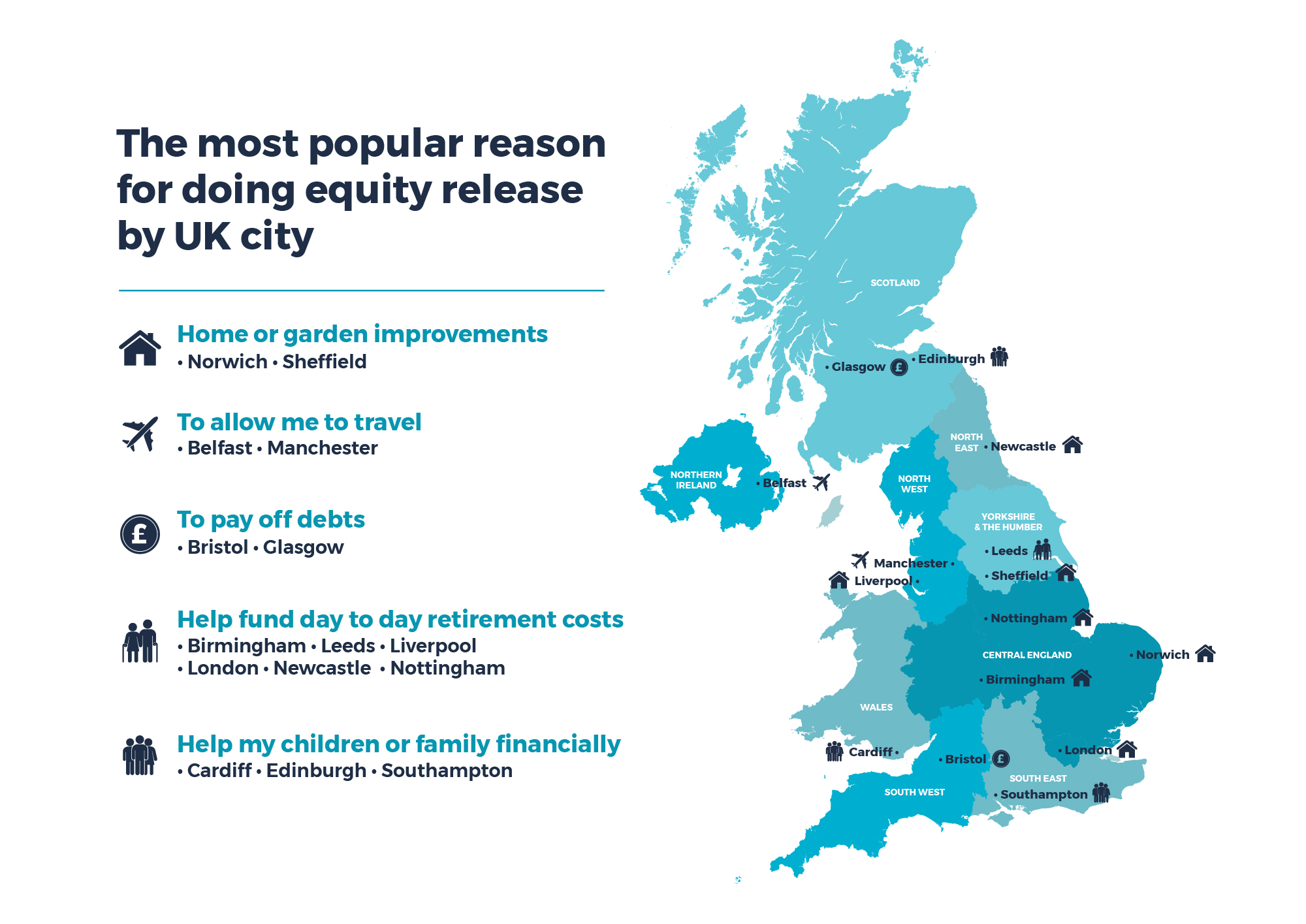

What would people in different cities spend their Equity Release money on?

Interestingly there were regional differences in priorities when it came to the reasons behind Equity Release.

Taking a look at 15 of the UK’s major cities, we analysed what the most popular reason for Equity Release was in each.

It seems homeowners in Belfast and Manchester are yearning to see the world, whilst those in Sheffield and Norwich dream about alterations at home to make staying local more appealing.

- To pay for home or garden improvements – Norwich and Sheffield

- To help fund day to day retirement costs – Birmingham, Leeds, Liverpool, London, Newcastle and Nottingham

- To enable travel – Belfast and Manchester

- To pay off debts – Bristol and Glasgow

- To help children financially – Cardiff, Edinburgh and Southampton

Overall, those in Northern England and Northern Ireland were twice as likely to want to use the money to travel, compared to those living in Scotland or the South West of England.

Home improvements were more popular in the South East of England than any other region. Clearing debts was most pressing for those in Northern Ireland and South West England.

Free consultations available in the UK.

Get Started NowDifferences in Men v Women using Equity Release

Geographic locations weren’t the only reasons for differences in opinion. Men and women also had different priorities in terms of how they would plan on spending the money.

Both ranked day-to-day living costs as the most common reason.

However, men were twice as likely as women to want to use the money to travel and three times more likely to want to do Equity Release to pay off other debts.

The top five reasons men would plan on using Equity Release are:

- To help fund day-to-day retirement costs

- To enable travel

- To pay off debts

- To help my children financially

- To pay for home or garden improvements

The top five reasons women would plan on using Equity Release are:

- To help fund day-to-day retirement costs

- To help my children financially

- To enable travel

- To pay for home or garden improvements

- To pay off debts

Overall our research showed that women were slightly more nervous about Equity Release in general and marginally more likely to have decided they would never take out an Equity Release product.

Men were twice as likely as women to feel that it is pointless keeping all your wealth tied up in a property and not putting it to good use when it’s needed.

Equity Release’s bad reputation

When researching the 1,000 homeowners we asked them additional questions around their feelings on Equity Release. Six out of 10 of the respondents (57 per cent) said they would never consider Equity Release.

When quizzed about why they felt that way one in five (18 per cent) said they had been put off due to horror stories they had heard or read about. One in 10 (10 per cent) also admitted they were worried about negative equity.

A further 22 per cent were concerned that they would no longer own their own home. However, these don’t have to be an issue with modern Equity Release products.

All plans approved by the Equity Release Council have a no negative equity guarantee, meaning you will never owe more than the value of your home and excess debt will not be passed on to your beneficiaries. For Lifetime Mortgages, which accounts for the majority of Equity Release is (over 95 per cent of our clients opt for it), you will always own your home.

With the less common Home Reversion Plan, part or all of your home is sold but you can stay there rent-free for as long as you choose.

You should always choose a company which is registered with the FCA and is a member of the Equity Release Council.

Misunderstandings around the products were high. Only 33 per cent felt confident they knew what Equity Release really entailed. Just 8 per cent said they understood the difference between a Lifetime Mortgage and a Home Reversion Plan.

It’s possible that not having a clear understanding of the products, combined with the historic bad reputation, is putting the target audience off seriously thinking about whether Equity Release could be of benefit to them and the lives they want to lead in retirement.

What Our Clients Have To Say

Considering family

During questioning, our research revealed that one in eight homeowners over the age of 55 (12 per cent) have been put off releasing equity held in their home because they’re worried that their families wouldn’t want them to.

Homeowners in Scotland were most worried that their families would disapprove (15 per cent) and those in the South West were least worried (9 per cent).

We also found that only 13 per cent of men and 7 per cent of women agreed that it doesn’t make sense to keep money tied up in property when it could be put to better use.

Given you can’t take your money with you, it seems that many feel they should leave the largest possible inheritance for their families, by way of a property.

Because many families feel awkward discussing money and death these can often be conversations which don’t take place, leading to assumptions on both sides.

Homes may also have to be sold to fund care in retirement, which is one reason we always recommend families talk about these things as early as possible, to avoid miscommunication and to make sure everyone is aware of the situation.

Anyone wishing to take out an Equity Release product has to receive legal advice to make sure they are fully aware of the implications and details of the product they are taking on, which is a very important and sensible precaution.

Is Equity Release right for you?

For those who need to free up some money in later life to enjoy their retirement, or to ease their or their family’s financial worries, it can be an ideal solution if the homeowner doesn’t want to sell their property. There is the benefit that the money is tax free too.

But key to it all is really doing your homework and making sure you understand the details.

Ensuring your broker and lender are part of the relevant regulatory bodies (ERC and FCA) is a good first step to finding a reputable equity release lender. Be clear on any related fees and details around repayment charges and having the right to remain and the right to move.

Taking advice is vital and a mandatory part of the process. But for many people Equity Release can provide some financial freedom and a way to make the most of the property market boom without having to move.

You can also watch this informative video we produced on Equity Release:

Gerard BoonB.A. (Hons), CeMAP, CeRER

Gerard is a co-founder and partner of Boon Brokers. Having studied many areas of financial services at the University of Leeds, and following completion of his CeMAP and CeRER qualifications, Gerard has acquired a vast knowledge of the mortgage, insurance and equity release industry.Related Articles

- Can I Sell My House If I Have Equity Release?

- Equity Release Companies To Avoid

- What Happens On Death With Equity Release?

- Can I Release Equity To Purchase A Second Home

- Releasing Equity To Help Child Buy Their First Home

- Releasing Equity To Help Child Buy Their First Home

- How Does Equity Release Affect Your Family

- Everything To Know About Equity Release

- Equity Release For A Buy To Let Mortgage

- How Much Equity Can I Release?

- What Is Home Reversion?

- How Much Does Equity Release Cost?