What is Home Reversion Equity Release? How Does it Work?

As people approach retirement age, they often review their financial situation to make plans for the future.

This might involve downsizing to move into a smaller property and freeing up some of the value in their current property, or they may look at alternative options such as taking out a lifetime mortgage or a home reversion plan.

These alternative options provide the opportunity to release equity without the requirement to move out of the home

- How does a home reversion scheme work?

- Is a home reversion plan right for you?

- How is a home reversion calculated?

- What is the difference between a home reversion plan and a lifetime mortgage?

- What are the advantages and disadvantages of home reversion plans?

- How is home reversion regulated by the FCA?

- Conclusion

How does a home reversion scheme work?

A home reversion scheme enables homeowners (usually over 60 years old) to sell all or part of their home to a plan provider to receive a tax-free lump sum or regular payments in return, whilst still living in the property.

It is basically allowing the homeowners to access the value of their property without selling up and moving into another home but they surrender all or part of the ownership of their home.

The homeowners would not be required to pay rent and can live in the property until they die or move into permanent care.

Different providers have different age minimums for home reversion plans with some setting the minimum age at 60 and others only providing to people aged at least 65 years old.

The amount that you can borrow largely depends on your age (generally the older you are, the more you can borrow), the value of your property and health/lifestyle.

If you agree to sell part of the property in a home reversion scheme then when the last homeowner dies or goes into long-term care, the house will be sold and the proportion agreed of the sale price will go to the provider.

Any remaining amount will then be left to your will beneficiaries.

Is a home reversion plan right for you?

Whilst a lifetime mortgage does not appeal to everyone due to the amount of interest it can accumulate, a home reversion scheme is suitable for people that do not want to risk reducing their family’s inheritance through the difficult to predict the value of the compounded interest on a lifetime mortgage.

Whereas a lifetime mortgage is impossible to accurately estimate the full cost of, as it is based on interest accumulating until you die, a home reversion plan allows you to ringfence part of your home’s value to leave in your will.

Therefore, you don’t have to worry about accruing interest that just keeps building up and eating into the inheritance pot.

If you don’t want to downsize and face the upheaval of moving home then a home reversion plan may well be very suitable, as you have a lifetime tenancy to remain in the property whilst still getting access to the value of your property.

For homeowners that want some additional financial security, maybe paying off some outstanding bills, a home reversion will allow them to do that.

The equity released from the home can then be spent on a higher quality of living for the last chapter of life, from taking holidays, to getting private medical care.

Some people choose a home reversion plan for helping their dependents to get on the property ladder by providing them with their deposit or giving them financial support when they need it most, rather than waiting until they inherit it.

By having the option of a lump sum, or choosing to have regular payments, you are able to have cash at your disposal to spend it however you choose to.

The regular payment option can provide extra income in addition to your pension, in order to afford more of the things that make you happy, like treating your grandchildren, going out for meals or to make home improvements.

If you currently receive means-tested benefits then you should check how a home reversion plan will affect your entitlement, as you could lose out on your benefits.

You also should factor in the possibility that you could die soon after taking the plan out, meaning that you would not get good value from the arrangement.

Free phone and video consultations are provided in the U.K.

Get StartedHow is a home reversion calculated?

When you arrange a home reversion plan, you will agree on a percentage of your property to be sold to the provider.

This will typically be between 25% and 100% but the amount you receive will not be the full value of that percentage, as you will effectively be paying a sum in exchange for the benefit of being allowed to live in your home for the rest of your life.

The amount that you are able to borrow will be calculated based on the age of the youngest homeowner, the value of the property and the health of the owners.

The provider calculates the owners’ predicted life expectancies using health information and the older they are, the greater the sum they will have available.

When the homeowners die, the house will be sold and the percentage of ownership remains the same as originally agreed.

This fixed percentage applies even if house prices fluctuate, so if your house value goes up, if you have sold 100% of your home then it is the provider that will benefit from the value increase.

If you still own a percentage, your beneficiaries will benefit from the increase on their share of the house but not on the part you sold.

See What Our Clients Have To Say

What is the difference between a home reversion plan and a lifetime mortgage?

The main difference between these two types of equity release is that with a lifetime mortgage you still own your home, whilst with a home reversion plan you sell all or part of your home.

When you arrange a lifetime mortgage, you are taking out a loan against your home that you will pay interest on, whereas, with a home reversion plan, you are selling a proportion of your home so not taking out a loan, therefore you have no interest to pay.

With both types of arrangement, you are able to remain in your home until you die or go into long-term care.

Lifetime mortgages are offered to people aged 55 and over, whilst home reversion plans are only available from 65 (or 60 with some providers).

If your house value goes up, with a lifetime mortgage, the increase will be factored into the sale amount that is used to pay off the loan and interest.

However, if you sell part or all your home in a reversion plan, you don’t benefit from the increased value on that proportion.

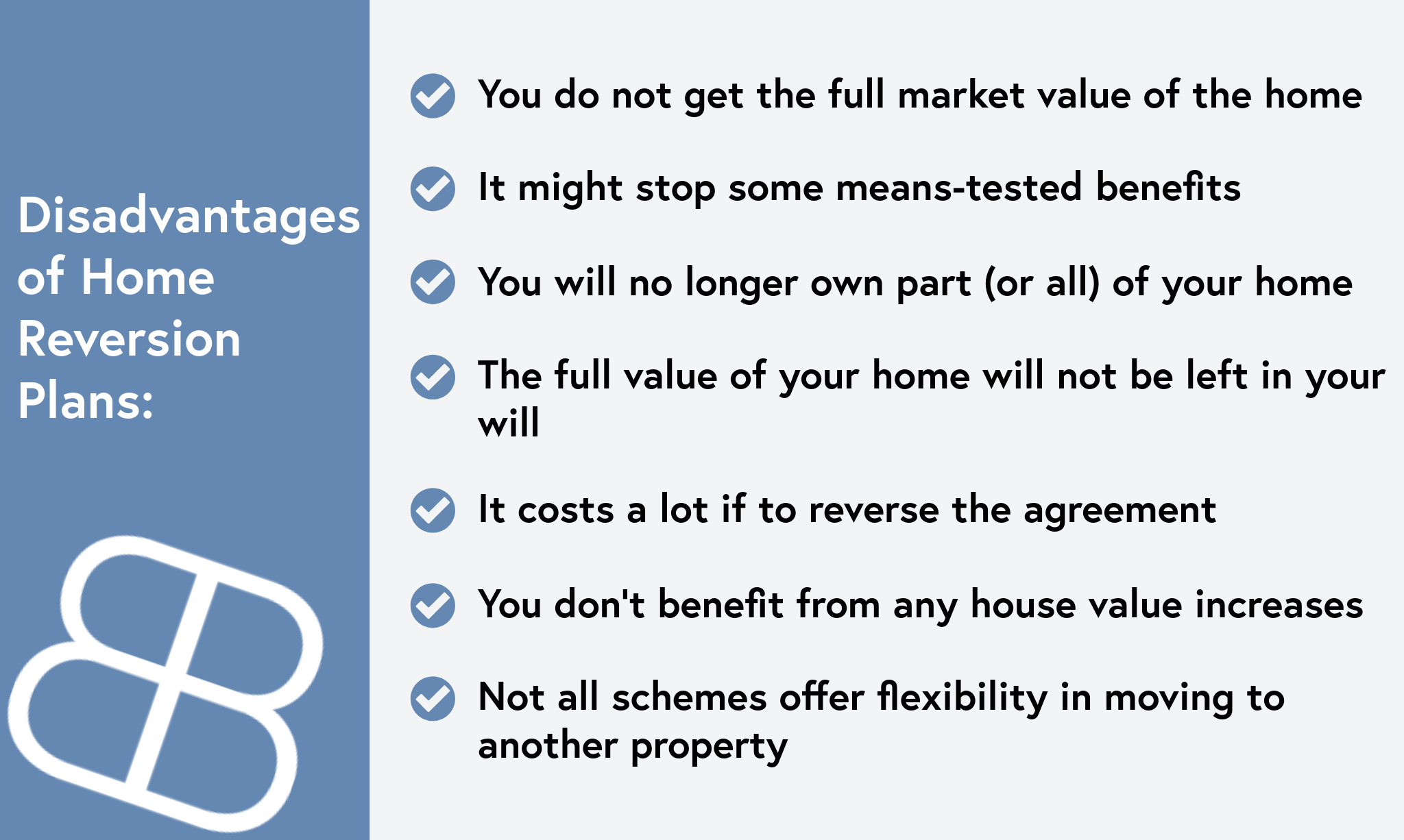

What are the advantages and disadvantages of home reversion plans?

There are many advantages and disadvantages to be aware of before you make your decision on whether a home reversion plan is the best option for you, including:

Advantages

Disadvantages

How is home reversion regulated by the FCA?

Equity release schemes have historically been a concern in regards to regulation but this has changed, as since 2004, equity release is now fully regulated by the FCA (Financial Conduct Authority).

Before you make your choice whether to take out any type of equity release, whether it is a lifetime mortgage or a home reversion, it is important that you check the provider is a member of the ERC (Equity Release Council) to benefit from the high standards they impose on their members.

Conclusion

Taking out a home reversion plan is not an easy decision and you will need to consider the impact it will have on the inheritance you leave, as well as whether it is the better option out of alternatives such as a lifetime mortgage.

Whilst the financial implications are considerable, with the right advice, you could stand to benefit from a better quality of life and never need to worry about money in your later years in life.

If you would like to speak to a reputable, trustworthy broker to discuss your options in more detail, call Boon Brokers today.

Gerard BoonB.A. (Hons), CeMAP, CeRER

Gerard is a co-founder and partner of Boon Brokers. Having studied many areas of financial services at the University of Leeds, and following completion of his CeMAP and CeRER qualifications, Gerard has acquired a vast knowledge of the mortgage, insurance and equity release industry.Related Articles

- Can I Sell My House If I Have Equity Release?

- How Much Does Equity Release Cost?

- What Is A Lifetime Mortgage?

- Everything To Know About Equity Release

- Can I Sell My House If I Have Equity Release?

- What Happens On Death With Equity Release?

- Can I Release Equity To Purchase A Second Home

- Releasing Equity To Help Child Buy Their First Home

- How Does Equity Release Affect Your Family

- Equity Release For A Buy To Let Mortgage

- How Does The Erc Protect You

- How Much Does Equity Release Cost?