The Mortgage Knowledge Crisis: First-Time Buyers Are Gambling With Their Financial Futures [April 2025 Study]

New research by Boon Brokers shows that 84% of first-time buyers don’t know how they can achieve the best interest rates, with 97% not learning about mortgages from school. Download the full research file in the footer of this article.

Key findings:

- 97% of first-time buyers did not learn about mortgages at school.

- 84% of respondents don’t know how to achieve the best mortgage interest rates.

- 93% of respondents don’t know what deposit is needed to secure the best mortgage interest rates.

- 82% of respondents don’t understand how a late payment will impact their credit file.

- 90% of 55+ year olds are unaware of how late payments affect their credit files

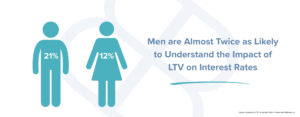

- 21% of men correctly identify that mortgage rates are affected by loan-to-value ratios, compared to just 12% of females.

Inspired by Santander’s study on the financial education of those leaving school, our research targeted first-time buyers with the aim to understand how this lack of financial knowledge translates into real-world decisions and the financial commitment of securing a first home.

The survey of 1,000 first-time buyers asked the basic questions surrounding mortgage interest rates, deposits, and credit scores, all with the objective to establish exactly what first-time buyers actually understand about mortgages.

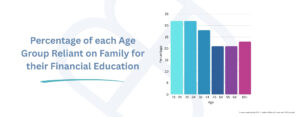

Our latest research demonstrates a clear lack of education, with 97% of respondents obtaining their knowledge on mortgages from outside an educational institution, and the vast majority relying on their families as a primary source of financial tutoring.

The Unreliable Nature of Generational Knowledge

Data shows that 23% of respondents admit to not learning about mortgages from any source, despite being first-time buyers, with the majority learning from their friends and family.

This lack of education is not limited to younger generations. The data also highlights that the older age groups show a worrying lack of financial awareness, with 40% of 55-64 year olds, and 50% of those aged 65+, are unaware of how late payments affect their credit files.

A primary concern in this trend is the accessibility of information. Naturally, research shows a decreased likelihood in older age groups to use online search engines or digital resources to fill gaps in their knowledge. This neglect of a proactive attempt to understand the financial world is becoming indicative of the current misinformation that is filtering through generations, reinforcing the cycle of poor mortgage and financial advice across multiple age groups.

Unfortunately, with the educational institutions not achieving great success with teaching a basic understanding of general finance, and even less about mortgages, the repetitive nature of relying on generational knowledge comes with significant risk.

Often shaped by outdated information, contextual societal pressures, and evidently a lack of formal education, the reliance on family members to provide accurate and helpful financial information is demonstrably leading first-time buyers astray.

When we begin to take a holistic view at the sources of education people use to learn, it comes with no surprise that we’re falling into a perpetual circle of misinformation.

Now, with the rise of ‘Tik-Tok’ learning and social media influencers offering quick ‘shorts’ of both unsolicited and unsanctioned financial advice, concerns are rising that the younger generations are at an increased risk of believing false facts.

An accessible source of truth is clearly missing for the first-time buyers of today, with no signs of correction in the foreseeable future. At best, research shows that we are looking at the start of a very worrying snowball effect, with the lack of financial education needing to be addressed before the volume of misinformation becomes unmanageable.

Regional and Gender Differences

Our research surveyed respondents from across the four regions of England. While all the research indicates a consistently low mortgage knowledge across all regions, respondents from the Southwest of England demonstrated a stronger understanding of the mortgage fundamentals compared to other areas.

At this juncture, the reasons for this disparity are unknown. Whether the foundations of mortgage advice are unintentionally ascertained through local initiatives, increased housing market dynamics, or economic factors – warrants further exploration.

Interestingly, however, gender differences also emerged from the survey, with 21% of men correctly identifying that mortgage rates are affected by loan-to-value ratios, compared to just 12% of women.

When we take a step-back and look at the abundance of research that demonstrates how the financial world is predominantly male dominated, The FTSE 100 companies only have 10 female CEOs for example, it is unsurprising that there is an imbalance in the incentive for financial education.

While the data shows that the financial knowledge of first-time buyers requires an urgent call for necessary change and a vast improvement in education around mortgages nationwide. Moreover, the report distinctly underlines the need for more gender neutral and inclusive financial literacy efforts.

The Fallout of Uninformed Financial Decisions

The data highlights the financial implications of this knowledge gap; 84% of respondents do not know how to access better interest rates, while an even more alarming 93% of first-time buyers don’t understand how their deposit size will impact their mortgage options.

This clearly shows how a lack of financial education isn’t just an inconvenience, but can quickly become a financial time bomb. Considering that first-time buyers don’t understand how mortgage rates work, the majority of first-time buyers are committing to one of the biggest investments of their lives unaware of the control they could’ve had over their now long-term financial strain.

“Loan-to-value is the key driver of mortgage interest rates. As a mortgage is the largest financial commitment that most people will ever own, it’s vital that the general public understand what dictates their mortgage payments. Without this knowledge, they may unknowingly agree to a mortgage with a higher interest rate than is necessary. For example, as interest rates change in 5% brackets, if someone has a 24% or 25% deposit, this could significantly impact their available interest rates. By just having that extra 1% deposit in this scenario, they may be able to access far lower interest rates.”

Gerard Boon Managing Director (B.A Hons, CeMAP, CeRER)

Misunderstanding The Debt Society

Despite living in a credit-driven society, 82% of respondents did not know how long a missed payment would show on their credit file.

The research further established the limited understanding that most first-time buyers have on their credit scores.

With an increase in ‘buy now, pay later’ (BNPL) products across different market places, alongside the societal pressures of having the latest smartphone, laptop, or car, the general attitude towards debt, repayment, and credit is becoming skewed.

Without the knowledge that a simple missed payment will last 6 years on your credit file, buyers are unknowingly damaging their creditworthiness when it comes to securing their own mortgages.

Crucially, as the majority of lenders use credit reports to assess your credit and financial standing before agreeing to loan a mortgage, a borrower’s credit score is a large factor that can determine lower interest rates and better mortgage terms.

A Vicious Cycle of Financial Misinformation

We’re now living in the mortgage knowledge crisis. While the study identifies a clear issue in the foundational knowledge of mortgages and how they’re determined amongst first-time buyers, it reflects a wider issue with misinformation at the centre of a vicious circle.

With only 3% of respondents receiving any formal mortgage education in school, young buyers today are left to rely on the outdated generational knowledge of family or listen to the ill-informed influencers on social media.

This research only scratched the surface of the fundamental knowledge all adults and first-time buyers should have, and demonstrates that the gap in knowledge is growing. This is leading to poor financial decisions, from failing to secure competitive mortgage products and interest rates to unknowingly damaging your creditworthiness.

This cycle of misinformation is perpetually repeating itself, with today’s first-time buyers passing their misunderstandings onto the next generation, and so forth.

Notes to Editors

Research was conducted between 21st and 28th March 2025 amongst 1,000 applicants, all of whom were first-time buyers.

About the Researcher:

The Researcher for this article is Gerard Boon (B.A Hons, CeMAP, CeRER). Mr. Boon is the Managing Director of Boon Brokers Limited, a Directly Authorised Online Mortgage, Insurance & Equity Release Brokerage in the U.K. Boon Brokers boasts over 9,000 clients across the country and is quickly scaling year on year. Mr. Boon is passionate about Artificial Intelligence in the industry. During his studies at the University of Leeds in 2018, he achieved a First classification for his dissertation project titled “Artificial Intelligence in Financial Intermediation: An Investigation into the Prospects of Robo-Advice Developments for Independent Mortgage Brokers in the United Kingdom”. Since 2018, AI technology has rapidly developed. Mr. Boon is hoping to update his research on the topic following this survey.

Download the Full Results of the Mortgage Foundational Knowledge Survey